Stablecoins: Rewriting the U.S. Debt Playbook

- Unity Investments

- Aug 18, 2025

- 8 min read

Stablecoins enable the settlement of payments on a global scale in a fast and secure manner. The industry as a whole has issued US$250 billion worth of coins and is now the 18th-largest external holder of U.S. Treasuries.[2] In this white paper, we assess 1) the accelerating adoption of stablecoins, and 2) what it means for U.S. Treasuries, the yield curve, and the broader credit ecosystem.

What are stablecoins?

Stablecoins, such as Tether and USDC, are tokenized cash issued by institutions on public blockchains. They promise stable value relative to fiat currencies through support from verified reserves. Following the passage of the GENIUS Act, which we will discuss throughout this paper, U.S. issuers are required to maintain one-to-one reserves in highly liquid assets, such as cash or U.S. Treasuries, thereby pegging one coin to one U.S. dollar.

Why do stablecoins exist?

Unlike traditional payment infrastructure, digital currency enables immediate transactions with minimal costs. Additionally, there is greater transparency in the number of intermediaries, 24/7 operating hours, and automated compliance processes. Above all, stablecoins are now asset-backed by highly liquid and redeemable collateral, mostly in the form of short-term Treasury Bills and cash. The current iteration of asset-backed stablecoins differs from the previous algorithmic, mint-burn stablecoins, such as TerraUSD, which we explain below. As they stand today, stablecoins simply provide global access to the digital Dollar, making them a trustworthy alternative to volatile currencies, especially in developing regions with limited banking infrastructure.

New vs. Old

Currently, Tether and Circle are the two largest stablecoin issuers globally, with a combined market value of US$227.2 billion in issued coins (see Table 1).[4][5] Tether and Circle approach stablecoin issuance strategy differently. Tether, or USDT, primarily serves as a utility for trading, remittances, and a store of value in volatile markets such as crypto exchanges. Tether’s reserve portfolio is more diverse, with a willingness to include volatile assets such as Bitcoin and gold.[4] Last year, Tether earned 54% of its revenue from interest on its treasury holdings.[12]

Circle, or USDC, prioritizes transparency and a compliance-first strategy. Circle’s reserves are low-risk and entirely backed by U.S. Treasury securities or cash held at regulated financial institutions.[5] Last year, Circle earned 95-99% of its revenue through Treasury interest.[12] As a result, USDC is likely better positioned for institutional adoption in real-world applications and is widely used in decentralized finance (DeFi) lending protocols. Recent big-name partnerships include Shopify for merchant payments, Ripple for XRP ledger integration, and Grab for Web3 customer experience.[12]

Compared to previous versions of “stablecoins,” TerraUSD, USDT and USDC are truly asset-backed and more stable. On the other hand, TerraUSD followed an algorithmic arbitrage, mint and burn mechanism pegged to Luna, another cryptocurrency, rather than material, fiat reserves. This made the coin vulnerable to a negative, reflexive spiral if the peg broke. In May 2022, this risk played out spectacularly, ultimately wiping out US$40-60 billion of TerraUSD, Luna, and their related ecosystem.[7]

Impact on U.S. Treasuries

The stablecoin supply has ballooned to an estimated US$250 billion, more than double the sum just 18 months ago. [1] Tether and Circle are the two largest issuers, collectively holding around 90% of all dollar-pegged stablecoins (see Table 1). The industry is now the 18th-largest external holder of U.S. Treasuries. [2] Moreover, this number is expected to reach US$2 trillion by 2028. [3]

As of August 12th, 2025, the total outstanding U.S. Treasuries amount to US$37.0 trillion, with US$29.6 trillion held by the public (see Table 2).[8] The stablecoin market’s share of U.S. Treasury Bills currently only hovers around 2-3%. However, if net circulation were to reach the forecasted sum of US$2 trillion, then stablecoins would collectively own ~30% of U.S. Treasury Bills, which could significantly impact the front-end, short-term interest rates of U.S. Treasuries.

What does the GENIUS ACT change?

In the years prior, the U.S. had no comprehensive framework to govern stablecoins. Instead, regulations were fragmented and undefined, with various agencies (SEC, CFTC, FinCEN) asserting jurisdiction over specific activities. There were overlaps leading to legal uncertainty and a lack of guidance, eventually leading to situations such as the TerraUSD collapse.[7]

Passed on June 17, 2025, the GENIUS Act mandates a one-to-one ratio between coins issued and reserve assets.[6] Notably, U.S. Treasuries are explicitly stated to be applicable for reserve assets. Furthermore, the act requires issuers’ holdings of Treasury securities to have a maturation period of less than 93 days.[6] The last requirement has far-reaching ramifications that would lead to outsized demand for shorter-duration Treasury Bills vis-à-vis medium- and long-duration Treasuries. As a result, we expect 1) a compression of short-duration yields, and 2) the steepening of the rates curve. This is already evident in the recent yields on 2-month and 3-month Bills, as they have dipped to near the Fed’s rates (see Figure 1) even after the Fed’s announcement to increase Treasury issuance in Q2 of this year, a move that typically would alleviate the supply shortage.[14]

As a tangential note: the uncharacteristic yield spike from July to August for the 1-month T-Bill in Figure 1 occurred despite the downward pressure provided by stablecoin buying, primarily because of a substantial jump in offering amounts at recent auctions. On July 3rd, US$55 billion was offered with US$115 billion outstanding at the time; the number grew to US$100 billion on August 14th despite US$200 billion worth of Bills that are currently outstanding.[10]

Figure 1. Data retrieved from U.S. Department of the Treasury.[13] Rates of 1-month, 2-month, and 3-month U.S. Treasury Bills over time (Highlighting the timeframe for current Fed rate). The vertical blue dashed line represents the enactment of the GENIUS Act.

Another concerning point to mention is Tether's reduction in purchases of long-term Treasury Bonds from US$65 billion in Q1 to just US$7 billion in Q2.[4] This pivot is a reaction to the GENIUS Act coming into effect and leaves a potential void in the long-term Treasury market.

Impacts on the broader credit ecosystem

The growth in issued stablecoins will lead to additional demand for short-dated U.S. Treasuries. In the face of China and Japan selling U.S. Treasuries for geographical considerations, the GENIUS Act, which enabled the rise of stablecoins, should alleviate upward yield pressure caused by the selling. China and Japan currently hold US$761 billion and US$1,135 billion in U.S. Treasury securities. This is down from their peaks at US$1,317 billion and US$1,328 billion in 2013 and 2021, respectively (see Figure 2).[15][16] A closer look shows stablecoins were already among the top buyers of Treasury Bills in 2024 at around US$40 billion, comparable to China’s US$43 billion and Japan’s US$22 billion.[18]

Figure 2. Data retrieved from U.S. Department of the Treasury.[20] China and Japan’s monthly U.S. Treasury holdings over time (2011~2025).

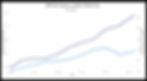

That being said, if the yields of Treasury Bills continue to compress, money market funds (MMFs) will likely search for other higher-yield alternatives, thus, bumping yield back up. MMFs primarily invest in short-term, highly liquid debt instruments. Currently, MMFs hold assets totaling US$7.2 trillion, out of which US$5.8 trillion is held in government securities. Specifically, most MMFs invest in Treasury Bills, repo agreements, and agency securities.[17] In 2024, MMFs purchased over US$75 billion worth of Treasury Bills.[18] Figure 3 shows that the net assets of MMFs begin to plateau at the beginning of this year, whereas Tether’s market capitalization continues to soar, suggesting the handover has already begun. This dynamic may dampen the true, net positive impact of stablecoins.

Figure 3. Data retrieved from ICI[17] (Weekly, April 2025 onwards), FRED[21] (Quarterly, until Q1 2025), and Coingecko[9].

Challenging to bank deposits

As for banks and other lenders, the arrival of stablecoins is a direct threat to bank deposits, the cheapest form of funding for financial institutions. Lost deposits will have to be replaced with higher-cost funding, essentially undercutting the industry’s net interest margin (NIM). For example, as of July 2025, the U.S. average savings account rate is 0.38%.[19] This rate tells us two things. First, deposits remain the cheapest form of funding for banks. Second, the current savings account rate is the lowest since the Fed rate dropped to 4.33% at the start of the year, suggesting that banks are slowly reducing rates to maintain their NIM. We believe that over time, it is inevitable that stablecoins will begin to compete away bank deposits. The final effect remains to be seen.

Conclusion

The GENIUS Act is set to take effect either 18 months from the date of enactment or 120 days after federal agencies issue final regulations; however, the fast adoption of stablecoins has already started to reshape the dynamics of the U.S. credit market. By driving demand for Treasury Bills, stablecoins 1) shift the front end of the yield curve lower, and 2) steepen the yield curve by moving away from longer-dated Treasuries. Yet, the overall net impact of stablecoins over time remains to be seen because of the complex relationship among the different players in the market, from banks to MMFs to stablecoin issuers.

If you would like to learn more about how we think about credit, yield, and related topics, please feel free to reach out to us at IR@unityinvestments.com. This is Life, Compounded.

References

[1] McKinsey & Company. (2025). The stable door opens: How tokenized cash enables next-gen payments. McKinsey & Company.

[2] Fortune. (2025, August 9). Circle, Tether stablecoins, Treasuries, and the U.S. economy: Impact of the GENIUS Act. Fortune.

[3] ABA Banking Journal. (2025, July). How stablecoins could affect borrowing costs for the government, businesses, and households. American Bankers Association.

[4] Tether International. (2025). ISAE 3000R opinion on Tether’s reserves. Tether International.

[5] Circle. (2025). USDC attestation report – June 2025. Circle.

[6] The White House. (2025, July). Fact sheet: President Donald J. Trump signs GENIUS Act into law. The White House.

[7] Dark, C., Rogerson, E., Rowbotham, N., & Wallis, P. (2022, December 8). Stablecoins: Market developments, risks and regulation. Reserve Bank of Australia Bulletin.

[8] U.S. Department of the Treasury. (n.d.). Debt to the penny. Fiscal Data.

[9] CoinGecko. (n.d.). Tether (USDT): Price, market cap, and information. CoinGecko.

[10] U.S. Department of the Treasury. (n.d.). Auction announcements, data, and results. TreasuryDirect.

[11] U.S. Department of the Treasury. (n.d.). Summary of Treasury securities outstanding. Fiscal Data.

[12] Chavanette. (n.d.). The stablecoin comparison of giants: Circle and Tether. Chavanette.

[13] U.S. Department of the Treasury. (2025). Daily Treasury yield curve rates.

Treasury.gov. https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_yield_curve&field_tdr_date_value=2025

[14] Reuters. (2025, June 24). U.S. bond market braces for surge in Treasury supply in second half of 2025. Reuters.

https://www.reuters.com/business/us-bond-market-braces-surge-treasury-supply-second-half-2025-06-24/

[15] CEIC. (n.d.). China holdings of U.S. Treasury securities. CEIC Data.

[16] MacroMicro. (n.d.). U.S. Treasury bonds major foreign holders: Japan. MacroMicro.

[17] Investment Company Institute (ICI). (n.d.). Money market fund statistics. ICI.

[18] Bank for International Settlements (BIS). (2025). Annual economic report 2025. BIS.

[19] Federal Deposit Insurance Corporation (FDIC). (n.d.). National rates and rate caps – Previous rates. FDIC.

[20] U.S. Department of the Treasury. (n.d.). Treasury International Capital (TIC) system.

[21] Board of Governors of the Federal Reserve System. (n.d.). Money Market Fund Assets, Quick Assets, Other (MMMFFAQ027S). FRED.